LIBERTARIAN PATERNALISM: WHY IT IS IMPOSSIBLE NOT TO NUDGE

RICHARD THALER: Here is the way Sendhil Mullainathan and I have thought about the day and a half that we have here. We have a pretty good idea of what we would like to do for the first three of our six sessions. This first session will be an overview of the concept of libertarian paternalism and choice architecture. The second one will flow directly from that, and has an idea, a solution, and we're going to talk about the problem that it may or may not solve. Then after lunch Sendhil is going to talk to us about some of the work he is doing on poverty.

That will leave us three sessions that are up for grabs and we will give you a menu. I know Jeff Bezos doesn't like to have to choose, but Nathan Myhrvold is going to vote twice. We will give you a menu of things. Danny Kahneman has a couple of things he has available to talk about and so do Sendhil and I, but we also felt like since we have the enormous luxury of nine hours here, if we don't quite finish one session we can pick up where we left off if that seems like a good idea.

Let me start by saying what behavioral economics is, and offering a definition. If Danny and I are the fathers of this field, then Herb Simon is the grandfather. He uses a great word, "pleonasm." How many people here know what that is? It's a redundant phrase. What he is saying is, why do we need a field called, behavioral economics? Isn't behavior what economics is supposed to be? Then Simon says the answer to why we need such a field, lies in the restrictive assumptions of traditional economics.

What are they? We refer to two kinds of creatures, Humans and Econs. Econs are homo economicus. We often refer to Human Beings characterized by Homer Simpson, and Econs by Mr. Spock. Those are kind of the right views. How do Humans and Econs differ? The first, and this phase is due to Herb Simon, is bounded rationality, and I want to include bounded attention.

In standard economic theory, humans are considered to be unbelievably smart. In fact, they are as smart as the smartest economist. Okay, that is not unbelievably smart‚ I'm contradicting myself already. But here is the sense in which that is true. Over the last 50 years, a norm developed. Suppose Paul Romer writes down a model of behavior of which the agents are pretty smart, but then Sendhil comes along and thinks of way in which the agents could be even smarter.

Then it's taken that Sendhil is smarter than Paul—and that his model is better than Paul's, and thus the agents just grow in intelligence with the cleverness. Since young guys are smarter than old guys, the IQ goes from me to Paul to Sendhil. The field has developed in a funny way where the agents get more and more unrealistically smart. Of course, we humans have limited brainpower. We have slow processors with frequent memory crashes. Nobody thinks that's a good description of how people think, so one of the things that behavioral economics has been trying to do is incorporate lessons from psychology about how the mind works and how real humans think, and replace Econs with a more realistic description of Humans.

The second feature of Econs is that they have no self-control problems. They eat just the right amount of food. They exercise just the right amount. They never have a hangover, and they have no need for New Year's resolutions. Real humans, at least since the time of Adam and Eve, have self-control problems, especially men in the presence of women and snakes, and apples.

A second aspect of behavioral economics has been to try and say how can we incorporate this idea that people have self-control problems into our description of an economy? The third is not really a problem. Economic theory has traditionally described agents as unboundedly unscrupulous. Econs view every opportunity as a strategic one. If I ask Jeff Bezos what time it is, and he's a human he looks at his watch and he says, 10 to 10‚ if he's an Econ, he says, hmmm. How could I possibly gain by giving false information here?

DANNY HILLIS: Jeff does do that.

THALER: Right. He may be an Econ. If you're the sort of person that when somebody asks you for directions, you point them in the right place, then you are more of a Human than an Econ. Actual humans are a little nicer than economists give them credit for. Econs will behave truthfully if it's in their self-interest to do so, but they have to figure out in every possible case whether it is. Sometimes it will be rational to tell people the correct time, but you will always be calculating whether that's a good thing or not. The last thing has nothing to do with humans and Econs. It has to do with markets.

From the beginning, behavioral economics has been economics. Danny Kahneman will remember in the very early years there were some competitors who had a very different agenda, which was to destroy economics and replace it with something else. That was never our agenda. Our agenda was to work very much within the economics paradigm and enrich it and expand it. We are big believers in markets but markets don't always work the way they are supposed to, and so one of the things that we will be talking about is what is the role of markets, when do they help and when do they hurt?

For today, I am not going to talk about whether markets are efficient; I am going to show one picture. I claim this is the single most convincing evidence that the law of one price doesn't necessarily hold. This is a photo that was taken in Buenos Aires.

Some economists have argued that this is not a violation of anything. This is price discrimination against Americans who are too stupid to know the Spanish word for orange juice, and to instance to notice that the photograph is identical. Nonetheless, economic theory says we shouldn't have that. That's all I'm going to say about financial markets for now. We can have as much more on that subject as you want.

The approach that Cass and I advocate is something we call 'libertarian paternalism'. Both of these terms are extraordinarily unpopular in our country right now. There are a lot of libertarians in the neighborhood of Chicago where I work and a few rural counties of Montana, but otherwise libertarians are hard to find. But they are popular compared to paternalists, whom everyone hates.

Here is our idea: take two reviled concepts that are contradictory, and combine them. We think they are lovable. By libertarian all we mean is protecting individuals' right to choose. By paternalism we mean improving the welfare of people as judged by themselves. If somebody asks you, what are the directions to get to the museum and you point them in the right direction, you are a paternalist according to us. We're not saying you should go to that museum, but if you want to go to the museum, it's over there, it's not over here.

At some points we refer to our approach as 'one-click paternalism'. I'm a little worried that Jeff will sue me if I use that, or he will take out a patent on it. But the idea is that we are trying to devise policies where we nudge people in the right direction, in the direction we think they will think is in their best interest. And the cost to them of opting out is one click.

We don't always get to one click. Sometimes the cost of opting out will be more than one click, but if you can think about what we are striving for, it's one-click paternalism. How do we get there? We get there with something that we call 'choice architecture', and that is what I will talk about in this first session, choice architecture.

Who is a choice architect? Everyone in this room is a choice architect. Anyone who designs the environment in which you choose is a choice architect. If you go to a restaurant, there is a menu. Somebody thought about how to structure that menu. In many restaurants you have appetizers, then main courses. In some restaurants the main courses are divided into meat, fish and pasta. In others they are all mixed up. Sometimes they are arranged in order of price. Sometimes there is no apparent order. Everything we know about psychology tells us that all of those things matter. Everything matters.

If you start with that as a premise, that everything matters, that all the tiny incidental features of the environment influence what people choose, then the choice architect has control of all of those features that can influence what people do.

Consider the following thought experiment. Suppose the head of the school cafeteria runs an experiment and discovers that the order in which the food is displayed influences what kids eat? That is certainly true. What use should she make of that information? She now knows that simply by putting the apples before or after the Twinkies, she will influence the percentage of apples and Twinkies that the kids eat. Should she arrange the food to make the kids, say, as healthy as possible.

That's one possibility, but there are many others. She could try to fatten the kids up. Maybe she has a fat kid and her kid gets picked on at school and she thinks that if the other kids are fat then her kid won't be picked on as much. That is an option. She could take the principled stand that would appeal to some of my colleagues that she should arrange the food at random so as to avoid influencing what people eat, though of course she would be fooling herself into thinking that she was avoiding that because a random selection will influence kids compared with some other arrangement, and in fact it will also make the cafeteria a nightmare. If the food is arranged at random, you're never going to be able to find anything.

Or she could try to maximize her own income by featuring the items for which she gets the largest bribes from suppliers. You can make an infinite list. Here is one that economists have been densest about understanding. Maybe it's just my colleagues. Even some of Paul Romer's colleagues have problems with this point. You have to pick something. There is no such thing as neutral choice architecture any more than there is neutral architecture. Somebody designed this building that we are in. They had to make choices: where is the door, where are the windows, where is the bathroom? That's true fore every building. The building that the new Chicago Business School is in is a beautiful new building. The architect had one block to put the building on and a bunch of constraints. There had to be 170 offices, 12 classrooms and so forth and so on, but then he had a blank slate about what to do.

All kinds of small things about the architecture influence the way people use it. For example, there are open stairwells that connect the floors the faculty are on, with a big skylight above them. That open stairwell makes the colleagues on adjacent floors feel like neighbors in a way in which they don't in a building where you have to take an elevator or go into a claustrophobic stairwell. They also get a little more exercise because people always want to use those stairs. They never take the elevator. But if they have to go to one of the floors without an open stairwell, they jump in an elevator.

If you remember one thing from this session, let it be this one: There is no way of avoiding meddling. People sometimes have the confused idea that we are pro meddling. That is a ridiculous notion. It's impossible not to meddle. Given that we can't avoid meddling, let's meddle in a good way. Some ways of meddling are better than others. This is taken from a wonderful book that you guys should all know by Don Norman called The Design of Everyday Things. Here is my favorite example from the book. This is a picture of the urinal in the Amsterdam airport. We have seen this now in Munich, Moscow and Singapore. Here is a blowup.

MYHRVOLD: I have one in my house.

THALER: Do you? There is a company that gives the decals away now.

MYHRVOLD: But the best ones are baked in because the details come off. They sent a whole white paper and it's Die Target Flei in German.

THALER: Here's an interesting bit of psychology that I stole from Paul Rozin. Here's the fly that has been baked in. If I touch it, it grosses people out. Like, he doesn't want to shake hands with me. It's okay to pet the elephants, but if you touch the fly people get grossed out. I don't know whether you know this but the guy who came up with this was an economist. He got the idea to etch those flies into the urinals and claims that it reduces spillage

MYHRVOLD: "Overspray" is the term. It turns out that the big deal in airport urinal maintenance is overspray. It's basically how much you have to mop up the walls and the floor from this disgusting and corrosive substance. There's a huge reduction.

THALER: In my mind this fly has become the metaphor for what Cass Sunstein and I mean by the word "nudge". My definition of a nudge is a small feature of the environment that attracts our attention and in so doing alters our behavior.

Notice, no one is being forced to aim at that fly. I'm waiting for the evolutionary study. It's got to be that there is an evolutionary reason that if you give men a target they will aim at it. But whatever the reason is from the savannah, that is true. This is libertarian paternalism at its best. It costs nothing. It saves tons of money and doesn't make anybody do it. That is in one picture what the enterprise is about. Let's get to a little bit of substance.

These are the principles of good choice architecture. My sense is that most you guys probably know all of this at some level. But this will give us a structure to use to think about these concepts. The first one is defaults. A default option, as you know, is what happens when you do nothing. Normally when you do nothing, nothing happens, but in some situations when you do nothing, something happens. If you leave your computer on long enough, the screen saver comes on. How long it takes for that was a default option that the computer manufacturer set and most people never change.

The TV networks have spent a lot of money thinking about the order in which shows should appear because there is enormous spillover‚ a different kind if spillage. If you watch one show, the next thing you know you're watching the next show, although the costs of switching are one thumb click. The main empirical lesson from lots of research on this is that defaults are very sticky.

An example of this is organ donation. We know that the number of organs you get depends on what the default is. Here is a problem with an opt-out method of organ donation. The survivors are typically given veto power over the donor's wishes, either implicitly or explicitly. For example in France they supposedly have presumed consent, but the doctors always ask the survivors if they have any objections to harvesting the organs. The evidence suggests that if the donor has only implicitly given his preferences, the survivors are more likely to overrule those preferences. The method that I now advocate is what is called 'mandated choice'.

If you get your driver's license renewed in Illinois there is a box you have to check, donor or not donor. That makes the cost of doing something zero. You have to check a box to get your license, so you check one, and now the decision has been made at least a little bit more active and I conjecture that we will have fewer overrules as a result. We will have fewer potential donorstan in an opt-out system because some people will say no, but my guess is that we will have more organs.

The second principle is to give feedback. The first thing we learn from psychology is people can't learn unless they get feedback. Here is one of my favorite examples. If you paint a ceiling white on top of white, it's very easy to miss a spot because you are not getting feedback on what you are painting. Some genius invented a white paint that goes on pink and then turns white. You can see what you are painting and then you don't miss a spot. Digital cameras, like the one Nathan has, have lots of advantages over film, one of which is that you immediately get feedback on the picture that you have taken. That prevents disasters like spending a day shooting having forgotten to load film in the camera or having not loaded it the right way.

One interesting change to cheap digital cameras is, in the original ones you would press something and nothing would happen. You got no feedback as to whether you took a picture. Now they've added a fake shutter click. The one on the iPhone is extremely satisfactory. It sounds like a single lens reflex. In fact, there is even an image of a lens closing. This is a way of giving people feedback that they pressed the right button, so that is a good thing.

Here is a more practical example. There is a device you can put into people's homes called an ambient orb. What it does is measure energy use and it glows. The more energy you are using, the brighter it glows. You haven't changed any prices, all you have done is given people feedback. In one experiment it reduced energy use at peak periods by 40 percent. You could make this even better by equipping it so that it would not only glow but also play some annoying music if you were using a lot of electricity. Abba is a good choice of annoying music but being a libertarian, I think people should be able to pick their own. Wagnerian opera would be my annoying music of choice, but then my wife might turn on the washing machine because she likes that.

The first time I went to Paris and went into the subway, you get one of these little tickets and you stick it in and it pops up the top. The ticket has a magnetic stripe on one side and some writing on the other and I wasn't sure which way to put it in, so I stuck it in with the magnetic stripe up and that worked, and for 25 years I was very careful about always doing it that way. Then I was spending a few months in Paris a couple of years ago and I was showing somebody around the Metro. I said you put the ticket in this way and my wife starts laughing and I said, what are you laughing at? She said it doesn't matter which way you put it in. Any way works, which is the reason why I had done it perfectly for 30 years because there was no way to screw it up.

Compare that with the parking garages in Chicago and probably many other cities where when you leave you pull up to some machine and you reach out with you arm enough to stick in your credit card to some slot. There are four ways, up, down, left, right; one way works. There is a sign there but it's somehow confusing, so you are very often behind some idiot or you are the idiot that is that is putting in the card in.

This is a combination of expect error and give feedback because if you put the card in and it spits it out and the gate doesn't go up, you have no idea what mistake you made. Was it the wrong card? Did I put it in the right way? I'm looking at the card and which way did I put it in? Right? You could make the same mistake again. It's gotten so bad that if you park in the garage at the Chicago Symphony‚ and this is a labor saving device, right? They pay people to stand by the machines after the concerts and put the cards in correctly because otherwise the patrons would be there for hours honking. Obviously you could build a machine that would read the card like the Paris subway. It would be a little bit more expensive but you wouldn't need to pay those people to stick the card in the right way.

I recently sent a chapter of a book to Hal Varian, who is the chief economist at Google, and said I think this stuff might be of interest to you guys. I got an email back from Hal saying, you forgot the attachment and by the way, if you were using Gmail, you would have received a message that says, did you forget the attachment? Well, it turns out this was not the case. A) He claimed that it was his idea, B) that is was in Gmail, none of which was true as far as I can tell. I think there was some beta version of Gmail that had this feature. But you can see the idea of it is good.

Here is an idea we've invented and we hope one of you guys is going to figure out how to implement it. We got this idea after having received an extremely rude email. The idea is we have all sent very emotional emails that we have regretted within seconds of pressing the 'send' key. The software we need is something that detects emotional-related emails. Eudora had some very bad version of this that detected curse words.

KAHNEMAN: Including the word "Dick".

THALER: Yes. We need something better than that, something that somebody in this room can produce probably by the end of the weekend. We need software that will detect emotionally laden email, and then you will get this message: this email appears to be emotionally laden, are you sure you want to send it? The default will be it goes to purgatory. You press 'send', it will go to purgatory, which is a file that will be very difficult to find on your hard drive. Then the default will be nothing, the email will never be sent. If you want to send it, you will have to go find purgatory, and you can choose how hard it will be to get it out of there. Maybe you have to solve some kind of Sudoku puzzle or something like that. But it will almost always be easier to write another email the next day when you're calm. I'm hoping one of you guys will invent that.

Here is something that Sendhil and I have discussed. Suppose you work for a drug company, you're a chemist, and you come up with some new compound that cures something. How often do you want people to take the pills? The best would be one dose that the doctor gives you and you are done for life. Right? There is no compliance problem with that. The next best is once a day in the morning because almost anybody can master taking pills as part of their morning routine. Twice a day is much worse especially if you are not supposed to take it before you go to bed because your evening routines are highly variable. You have carry pills around.

But frequency is not the right thing because every other day is a catastrophe and every third day there is no human, well, maybe my wife who is organized enough to remember to take a pill every third day. I could have a disease that would kill me if I didn't take my pills, and if I had to take my pill every third day I would die. There are some pills women take for osteoporosis once a week and once a week is manageable. Most take them on Sundays. You can see there is some interesting psychology lurking here behind a design issue and you would want to think about it. Drug compliance is a huge problem.

MYHRVOLD: There are some very clever ideas for this. One is a smart pill bottle that runs a lottery during this period. If you open it up within the appropriate period of time, you have a chance to win money. It works great in testing.

THALER: As long as people carry the pill bottle around.

MYHRVOLD: If you give people an incentive, that there is a lottery, that's an instant lottery. The LCD display will say 'you won' but only if you are opening it within that appropriate period. They don't know you took the pill but if you were there opening the bottle, probably you are going to.

THALER: Right. So long as the pill doesn't have side effects.

MULLAINATHAN: A case where this is extremely important is tuberculosis. Dick was saying, oh if it could kill you, you still wouldn't take it, but in reality tuberculosis can kill you and in reality many people die even though they get the medicine because they're not taking it. It also has consequences for the rest of us because it creates drug resistant strains. If you look at the adherence problem in tuberculosis it is massively important. One of the challenges with some of the solutions you are talking about is that they are extremely expensive.

If you look at a country where there is tuberculosis, the best method they have is what are called doctor's direct observation. They literally send someone to your house, watch you take the pill. In some countries labor is cheap so it works well. A technology solution would be fabulously useful if you could get the price point down. The challenges they have had are thinking about clever ways of getting that price point down.

MYHRVOLD: My company has done some work on this tuberculosis thing. The most disgusting thing about it is that there is effectively a market price in many of these countries in Africa for both the dry pill and the wet pill. The dry pill market is people who resell the medicine without taking it. The wet pill market is someone who pretends to swallow it while they are observed then takes it out and sells it. Is that sick or what? But in fact there are people who figure they are well enough and they would rather sell the pill to somebody else. Meanwhile, there is somebody else who for whatever reason can't get in the program and will buy a wet pill.

MULLAINATHAN: One of the reasons that this is related to the principle of feedback is that tuberculosis has this feedback problem. Long after you don't feel sick, you are still sick. It's at the late stage that compliance drops off. What would be great, even better than a pillbox that reminded you, is a device that showed you that you are still pretty damn sick. This could be a simple thing that you blew into that showed you that you don't have the breath capacity of your 80-year-old grandmother.

MYHRVOLD: That's simple to do because you lie basically.

MULLAINATHAN: Right. I'm pointing out that maybe feedback, as a solution here is different from compliance.

THALER: The same with antibiotics. People don't finish their dose. Maybe you would want a drug that doesn't cure you until you are done. Your cough doesn't go away until you have taken the tenth day of the pills because it's giving you some other little virus. (I'm being facetious here in case anybody didn't notice.)

The interesting point is that the solutions here are a mix of technology and design. If we could make the pill so you could take it once a month with an injection, which would solve the wet pill problem. Conceptually we can see, if they are selling it because there is a black market, that is a somewhat different problem than the problem we have here of people being absent minded.

MYHRVOLD: But in TB you need to go all the way unfortunately. If you are taking your Lipitor or your osteoporosis medicine, if you skip one, it hurts you but it doesn't hurt anybody else. The problem here is that you can hurt everybody else.

THALER: Right. Let's move on and talk about Save More Tomorrow.

The idea my colleague Shlomo Benartzi at UCLA and I had was many people say they would like to save more in their 401K but don't. A survey David Allison of Harvard and his team conducted found that two-thirds of participants say they are not saving enough in their 401K plans. Half of those announce an intention to save more next year and almost none of them do.

My Chicago economist colleagues would make fun of those statements of intention because they would say, so what? They think they should save more, what does that mean? If they think they should save more, then they save more. That's because they don't understand about will power. These statements of intention are not random. No one has ever made a New Year's resolution to smoke more next year, or to watch more sitcom reruns. When somebody says that they have this intention to do something, which creates an opportunity.

I helped my secretary quit smoking once. The first thing was to get her to say she wanted to quit because otherwise it's hopeless. It's the same with saving. Once people realize there is a problem, the first step is solved. Something Sendhil and I were talking about a little bit this morning, many people think that the solution to a lot of these problems is something called financial literacy. It's not. That's almost never the solution for lots of reasons that we will come back to.

Here is a good example where most people get it that they should be saving more and never get around to it. Our plan is very simple. We say to people, would you be willing to save more starting next year when you get a raise? Then that stays in place until you hit the maximum or you opt out. Almost nobody ever opts out.

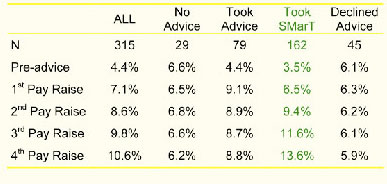

Here is what the data looks like in the first company where we did this.

If you look at it, this is a column of people who got no advice about what to do, and this demonstrates the inertia we see in most of these plans. The only reasons these numbers are changing at all are that we have some attrition in the data; some people are leaving the company. People are doing nothing.

These are guys where there was a financial planner who offered advice, suggesting you increase your saving rate by five percentage points. They do that and then they do nothing.

Here are our guys. This has now spread like a weed.

One of the themes that we are hoping to develop is how do businesses help or hurt in these things. Save More Tomorrow is spreading like a weed because the companies that administer 401K plans stand to gain by having people save more. It's not because they think I'm a nice guy or necessarily because they think people ought to save more, although they probably do. It's like Jeff thinks people ought to read more books but that is not what is driving him.

MYHRVOLD: Because he's an Econ.

THALER: Right. All of those companies quickly realize that stuff like this is good for people and happens to be good for their bottom line, and so it's basically available now in any company that has their 401K plans administered by one of these plans. If your companies don't have this, they should.

Mappings. Something we are going to be talking about in the next session, if you think about a one-line summary of the difficulties people have of making decisions, it's that they don't necessarily understand how their choice maps into the utility they are going to get. Suppose I buy an Amazon Kindle. Until I use it, I may not appreciate whether I'm going to enjoy the experience or not. It's much worse when you are choosing a mortgage. Very few people understand the difference between various mortgages. A good bit of choice architecture, and this is what we are going to talk about in the next session partly, is how can people better understand what they are getting?

Here is a visual of understanding mappings. As everybody knows, there are two dipsticks in most cars. It's very easy to put the wrong thing into the wrong dipstick. Here is a car that labels the engine oil dipstick with an "O" and the transmission fluid with a "T." Those don't cost any more than any other dipsticks but it solves that problem.

Mapping problems comes about when we don't know what we are going to get. When we go to an ice cream parlor if we order chocolate or coffee or vanilla we know what we are going to get. If we buy a European growth fund, we don't know knows what the transformation of that into our distribution of wealth in retirement looks like. Even if you knew that, what does that do to my utility? That is a difficult problem. That is the kind of problem where we need help. We'll talk about this more later.

Finally, and this also leads into what we are going to talk about in the next session, when there are lots and lots of choices we need to structure the decisions. Imagine we went to a paint store and had the paints listed in alphabetical order. You had Arctic White followed by Azure Blue. That would not be a good search model for paints. Instead we have something like this where we can see the paints and we can search using a color palette, this thing down here. Then we could even play with it. That's a good way of choosing paints.

I gave a talk in London that had a list of all the speakers that had given a talk at this place. Al Gore was listed right before Tim Harford. Can you think of what the rule was? It turns out they have speakers listed in alphabetical order by first name, which is already pretty crazy, and Al Gore was listed under "The Rt. Honorable", so he was under "T" and so right before Tim Harford. Not good. How can we structure complex choices?

If I were asked to devise a 401K plan now, it would look like this. First of all, it would be automatic enrollment. That goes without saying. And Save More Tomorrow. On the asset allocation there would be a default investment strategy, and probably my choice would be something called Target Date Fund, where they pick a fund that is based on when you are going to retire. If that is low cost, that is good enough.

The first line of the form would be, do you want the default investment strategy, yes or no? If yes, you're done. If no, now there is a small menu. Think about this like going and ordering wine at a restaurant. The first line would be, do you want us to pick a wine for you that will match your food, yes or no. If not, here is the one-page list of the sommelier's choices for what is drinking well now and good price value. Do you want one of those? No. If no, okay. Here is the 300-page list that I would enjoy spending an hour browsing through but most people wouldn't. That is the right way to do 401K plans and lots of similar things.

Incentives. We are still economists. Behavioral economists are still economists. We believe in incentives. But the behavioral twist on incentives is that we can make incentives more salient. For climate change, think about a thermostat that when you adjust the temperature, it tells you how much that costs. That is going to have a huge impact.

Think about why there is so much political uprising now about gasoline prices. It's because it's in your face. You fill your tank up, and you pay $80. It's used to $40. It's there. You go to the grocery store; most people don't know the price of most of the things they bought. They may have the sense that I could buy the family's groceries for a week for $200 and now it's $250. But they still don't quite know what prices have changed.

Sendhil has some interesting data that he'll talk about. The poor know more about this than most of us. The reason why gas prices are a political issue is it's in your face. If we want to alter behavior, we want to get the prices right, that is why we want a carbon tax or cap and trade, but we also want it to be in your face.

At the gym I love putting the power adapter on an elliptical machine, in part because it gives a massively inflated count of the number of calories burned. I was thinking suppose instead of calories it gave you a food item, you get cookies. Every 10 minutes you get another cookie.

The worst bit of choice architecture ever devised by anybody Intentionally is the Medicare prescription drug plan. The mantra of the people who devised it was maximizing choices. If you give people enough choice, then everything is going to be fine.

People have choice. There are 50 different plans in each state. They vary from state to state. There is a website that you can go to for help. The way you have to use this is you first have to type in a list of all the drugs you take. There is no spell checker. There is nothing like Google, "did you mean"? If you type Xanax and you spell it with a "Z" instead of an "X" you get "huh"?

Here is my favorite fact about the Medicare prescription drug program. There is a certain subset of participants who are eligible for Medicare and Medicaid, the so-called dual eligible. These are poor. They were forced to switch over, so the government had to choose a default. For everybody else, there was no default because it was purely opt in. If you wanted to join you had to sign up and pick one of these 50 places.

For these dual eligibles, since they are forced to choose, the government had to pick a default for them in case they didn't. What method do you think they used to pick a default? No one will guess it. Red. Some people think I am making this up or that George Bush did it just to make me happy. The reason was that the designers they had a philosophical approach that said we don't want to choose for you so they picked one at random.

The State of Maine did something intelligent, which is say we can guess which of these plans will be best because the drugs people take if you are old are very predictable. They are the drugs you take now. Or the drugs you take next year and the drugs you take now plus one.

It's very easy to forecast which of the plans is good and doing that, what is the number? It's about $500 a year, per person we can save by choosing a plan intelligently as opposed to picking one at random. Here is an interesting thing—the business angle here. This is sort of a lefty program‚ prescription drugs for everybody‚ that was devised by a Republican administration, so there is a big private sector component. The part that the government retained is the part that they are screwing up big time, like the website that doesn't have a spell checker. Just imagine if Google were running that website or Amazon. Just think of how much better it would be. Why wasn't that part privatized?

The intelligent assignment, again that part could be privatized very easily, and we're going to show you the way we can get there in the next session.

Why won't markets solve this problem? You can think of markets acting in two different ways. One is teaching and one is catering. Take the example of flight insurance, which only a few of us here are old enough to remember. In the old days they used to have a booth where they sold a life insurance policy good for one flight. It was a very dumb thing to buy. How would markets eliminate that? Econs don't buy flight insurance. Humans buy it because they are afraid of flying. Of course, this didn't guarantee the plane wouldn't crash but it got you a $10,000 life insurance policy that lasted for an hour.

KAHNEMAN: But you also know that if you don't buy it the plan will crash.

THALER: There is that. Let's think about markets here for a minute. How would markets eliminate this, you would stop people from doing this stupid thing. One you could think is that we will have competition. Let's suppose the actuarial cost of the policy is a dollar and they are charging $25.

You would think the price would be driven down to a dollar. Wrong. It costs a lot of money to have a booth in the airport that's manned by a human. That's expensive space, expensive labor. It costs $25 to sell that dollar's worth of insurance. No extra profits are being made there. We don't expect the profits. In a rational world that product doesn't exist. It's not that somebody is making too much on that. What is the other way that markets could work? Well, you can imagine somebody sets a booth up across the hall selling the advice, don't buy flight insurance. Of course, nobody would buy that. Nobody is selling the advice that tells you "don't buy my book".

BEZOS: I can think of one more, which is the kind of bundling with a more rational product like American Express bundling car rental insurance with the card. People perceive this as having higher value than the actual cost. We can give someone value perceived.

THALER: Exactly. That's very good. That hasn't eliminated the collision damage waiver policy. Sophisticated people no longer buy that.

MYHRVOLD: But in the case of the flight insurance, what is the problem you are trying to solve?

THALER: The question is, if people are doing something stupid, which is buy this policy, it could be that they are buying it because they know it is going to prevent the plane from crashing.

MYHRVOLD: Or is it peace of mind. It's a little bit like saying, are you also going to be asking, how can markets solve escapist fiction? Religion? Tell me how you are going to solve religion and I'll be interested.

THALER: No. I'm not going to let you draw me into that trap.

MYHRVOLD: This means I just won.

DANNY HILLIS: Then explain what traps you are trying to draw us into because we might just agree with you. My sense is you are trying to lead us to something we all agree to.

THALER: Yes. I would say no rational person would buy a load mutual fund. No rational person should have bought the kind of whole life insurance that was sold for decades.

HILLIS: What's the problem you are trying to solve now?

THALER: I am stipulating that as a financial product this flight insurance was a bad purchase because you could have bought life insurance that will cover you for the whole year for the same price.

HILLIS: We would all agree that that was a bad purchase.

THALER: I'm asking whether we should say not to worry, markets will come in and solve this.

HILLIS: But you solve the problem of people making bad purchases?

THALER: Yes.

HILLIS: But that 's Nathan's question. People spend their money on all kinds of things.

THALER: We are agreed. It's not irrational to buy a bad novel. We may think that it's irrational for people to take load mutual funds. We can't imagine a scenario where any sensible person would do that.

KAHNEMAN: That strikes me as odd because you have brand shampoo and then you have generic shampoo and they are side by side and they are identical and people definitely buy the brand shampoo. What are you going to do about that?

THALER: I'm getting attacked. I'm not saying that there is something we necessarily want to do about this. I think you're right. I don't think there is anything that I want to say here that anybody would want to disagree with. The point is that the way markets work is that they cater to what people want.

MYHRVOLD: What people want sometimes doesn't make economic sense but it may make sense in some other way because empirically they do it.

THALER: Or it may be bad for them and people buy cigarettes and you can either say that that's because they get a lot of pleasure from the cigarettes or they made a mistake in starting and now they can't get themselves unhooked.

KAHNEMAN: The reason you are running into resistance is you sound very paternalistic. If there is a libertarian element, some of us are not seeing it.

MYHRVOLD: Right. In particular it's an Econ. Now you're being the Econ.

THALER: All right. Let me switch to mortgages.

BEZOS: I'm just curious. What did happen to flight insurance?

THALER: Eventually it went away and it was because of the fear of flying has gone down.

MULLAINATHAN: Let me make a point. The reason this point is hard for people around this table to understand is it is aimed toward a belief that no one here has. That is the problem.

MYHRVOLD: Yes. We think it's a fairly silly belief.

MULLAINATHAN: But it's worth at least articulating the belief because even though in the shampoo example, which seems like a ridiculous belief, it is a belief that pervades very important public policy. Let me try and articulate that.

When we see people choosing let's say mutual funds, there is a belief out there that if the government simply mandates disclosure and gets out of the way that the market for financial advice, that appropriate disclosure by funds, all of that, will result in people choosing funds that are generally good for them.

HILLIS: Does anybody around the table have that belief?

MULLAINATHAN: Exactly. I don't think anybody has.

BEZOS: I don't want to delay the conversation but to take the shampoo example. Sometimes it is the right decision for people to buy the brand shampoo instead of the generic even if they are chemically identical. I know a lot about shampoo, you can tell.

THALER: You're using the wrong one.

MYHRVOLD: It's a very important personal decision that I make about my shampoo but the reason people buy a branded product because it's not worth it for them to do the research. A branded product reduces the cognitive load of making a purchasing decision. In a certain sense it's a very rational decision.

HILLIS: Let me jump ahead a step. Let's even jump to let's say we have thought about it and there is a decision that is good for society for people to make. Does anybody have a problem with us making it easier for people to make that decision? I don't think anybody around this table would have a problem with that.

THALER: No. Here are two other objections that maybe no one here will make. People tell me all the time, don't I realize that people who work for the government are also bound with irrationalism. Let me stipulate that this has occurred to me. Even people at the very highest level of our government sometimes are not the brightest bulbs.

The second way in which we are sometimes attacked is the slippery slope argument that, well, if we have automatic enrollment the next thing we will have is prohibition. This is a stupid argument.

I'm done. Before we take a break I want to say that I'm shocked that we only got into the ruckus at the end.

MYHRVOLD: We're being polite. John said he wanted at least fifteen minutes without interruptions.

THALER: This was intended to be the only real lecture of the day and a half and we're going to go at it from now on.

BEZOS: I have a question of verification on the definition of paternalism that you had toward the beginning. What was the antecedent for the word "themselves"? In other words, people making choices according to what they think is best themselves, is it the choice architect the antecedent for themselves or is it the person for whom you are making the choice?

THALER: It's the person as judged by themselves, the choosers.

BEZOS: The choice architect tries to get themselves into the shoes of the choosee or chooser.

THALER: Yes. When you said last night at dinner that you like going to a restaurant where they have a set menu, it's because you are happy to have the chef act as your choice architect.

BEZOS: The chef is putting himself in my shoes, not himself.

THALER: Right. Otherwise he goes out of business pretty quickly.

BEZOS: Right. Although I find Hollywood directors when they follow that model they make bad films. When they try to make films that they love for themselves, they make better films.

THALER: Right. It's very easy to make that mistake.

BEZOS: It's one of the failure modes of a certain kind of paternalism, that it's very hard to put yourself in somebody else's shoes.

THALER: Absolutely. There is a concept‚ hindsight bias, but there is a more general cognitive problem called "the curse of knowledge", which is if you know something, it's hard to put yourself into the shoes of the person who doesn't. You techno-wizards have trouble explaining to us how to turn on the machine or why it is difficult how to teach a kid how to tie their shoes.

There can be all kinds of problems in ascertaining what is good for people, but there is a huge amount of progress that can be made where that is pretty clear. In the Medicare case, it's a pretty good guess that people want to reduce the bills they pay. That, and good service, is probably most of it. Mortgages, it's only the money. There's nothing else there. If you could find a mortgage that dominates another one, you want it.

BEZOS: Or a credit card.

THALER: A credit card. That exactly leads into what we are going to start with in the next session.

MYHRVOLD: I have a question. The choice architect's scope, what they do, is pretty small compared to the choice of whether there is a choice at all. In the cafeteria example, you can say the order in which you put out some Twinkies matters. But you could also not have Twinkies. This is kind of a second-order thing.

THALER: Great question. I didn't have the objections from the left maybe because of where I come from. But it is possible for somebody to say, why stop at libertarian paternalism. Let's not have any Twinkies.

MYHRVOLD: That is a much more effective way of ensuring low Twinkies consumption.

THALER: Yes it is, much more onerous. The point of this enterprise is to say how far can we go in achieving social goals, some progressive goals, tying one hand behind our back and having no bans and no mandates and still achieving some progress towards those goals? There may be situations where we want to go further.

People say we tried nudging people against cigarettes for 50 years and then we banned smoking in public places. There are people, like Ed Glaeser, an economist at Harvard, who think that we've demonized smoking now, that we have gone too far in that direction. I don't know. Like I say, the goal here is to say, how far can we go with choice architecture? At a recent dinner somebody said, why are you so un-ambitious? I said suppose I can make people 10 percent happier in some sense with these methods. That's not bad.

MYHRVOLD: Okay. You're a marketing guy, though. In the context of a company there are usually people there to sell the products a company has, no matter what. Another set of people is trying to build the products.

MULLAINATHAN: One thing that is very important. This move against paternalism is not simply a philosophical move that has to do with wanting to preserve individual choice. It has one very serious consequence. It's hard to see this in the cafeteria example but it's easy to see this in the context of, say mortgages.

A 30-year fixed-rate mortgage is a good choice. Almost everybody would take a 30-year fixed-rate mortgage. As with Twinkies, you could imagine saying let's narrow that down. Let's make it very hard to take something other than that. While those types of decisions may make sense for today, they destroy innovation. They destroy our ability for someone to come in and say you know the 30-year fixed-rate is good but I have a great idea, why not have a housing price risk-insured mortgage? It's not 30-year fixed at all. It's a mortgage that pays out. When housing prices drop and on back end I insure it using REITs and markets.

MYHRVOLD: Hire a rating agency.

MULLAINATHAN: Exactly. I'm not saying it's going to work or not but I'm pointing it out. That's an example. What you are doing when you move down the choice of paternalism, you're not restricting choice by the consumer, you're preventing forces of the market from operating. That's the more compelling argument against these types of choice restrictions.

HILLIS: I would observe that with this group, we're all very resistant to being nudged by being told what you call the standard arguments that people have answered. You will do better with this group by stating where you want us to get to and then if we have arguments, they may be new and different.

THALER: Absolutely. I apologize for having the list of objections. Let's go have coffee.